1 Introduction

In both standard and behavioral theories of choice under risk and over time, the value of a risky or temporal prospect is typically modeled as a weighted sum of the utilities of its constituent elements. Thus, in the standard model of risk preference (von Neumann and Morgenstern Reference von Neumann and Morgenstern1944), the expected utility of a lottery is given by the probability-weighted sum of the utilities of its individual prizes, as evaluated by a Bernoulli utility function. Under expected utility, concavity of the Bernoulli function captures classical risk aversion, giving rise to a preference for more equally-distributed payoffs over states of nature. Analogously, in the standard model of time preference (Samuelson Reference Samuelson1937), the discounted utility of a stream of payoffs is given by the (exponentially-) discounted sum of the utilities of its individual payoffs, as evaluated by an instantaneous utility function. Under discounted utility, concavity of instantaneous utility captures resistance to intertemporal substitution, giving rise to a preference to smooth payoffs over time. Leading behavioral alternatives, such as rank-dependent utility and cumulative prospect theory for risk (Quiggin Reference Quiggin1982; Tversky and Kahneman Reference Tversky and Kahneman1992), and (quasi-) hyperbolic discounting for time (Laibson Reference Laibson1997; Loewenstein and Prelec Reference Loewenstein and Prelec1992), retain this underlying additive structure while relaxing the assumptions of linear probability weighting and exponential discounting, respectively.

In principle, risk aversion and intertemporal substitution describe conceptually distinct preferences. Nonetheless, in settings where both risk and time are present it is common—and perhaps even natural—to assume that Bernoulli utility for risk is one and the same as instantaneous utility for time. In standard theory, this gives rise to the model of discounted expected utility, which has been a workhorse model of economics dating back at least to Phelps (Reference Phelps1962). Alternatives to the standard model take divergent approaches to the question of whether interchangeability of Bernoulli and instantaneous utilities is maintained. On one hand, the class of recursive preference models developed by Kreps and Porteus (Reference Kreps and Porteus1978) and Epstein and Zin (Reference Epstein and Zin1989) set out precisely to break the nexus—described by Weil (Reference Weil1990, p. 29) as a “purely mechanical restriction ... devoid of any economic rationale”—between risk aversion and intertemporal substitution. On the other hand, prospect-theoretic models of time-dependent probability weighting (Halevy Reference Halevy2008; Epper et al. Reference Epper, Fehr-Duda and Bruhin2011; Epper and Fehr-Duda Reference Epper and Fehr-Duda2012) posit a relationship between probability weighting and hyperbolic discounting, under the assumption that a single function characterizes utility for both risk and time.

The question of whether utility under risk is interchangeable with utility over time is also a core issue in the design of experiments to elicit time preference, even though such experiments need not of necessity entail any interaction between risk and time. The primary objective of such studies is usually to estimate the parameters of a discount function. However, since choices are a product of both the utility and discount functions, it is necessary to allow for the possibility of non-linear utility.

Unfortunately, until quite recently there were essentially no known methods to elicit the curvature of utility outside the domain of risk. This resulted in the prevalence of two main approaches. First, Coller and Williams (Reference Coller and Williams1999) estimate discount rates under the maintained assumption that utility is linear. These estimates are potentially biased if utility is in fact concave (Frederick et al. Reference Frederick, Loewenstein and O’Donoghue2002, pp. 381–382).Footnote 1 Second, Andersen et al. (Reference Andersen, Harrison, Lau and Rutström2008) measure utility by eliciting subjects’ risk preferences, and combine risk and time preference data to jointly estimate a discount function adjusted for the curvature of utility. This assumes that utility under risk also represents utility over time; it is found that adjusting for this degree of curvature results in substantially lower discount rates than when utility is assumed to be linear.

The objectives of this paper are twofold. First, I introduce a novel experiment design that allows a clean comparison of the curvature of utility elicited under risk (in the absence of delay) and over time (in the absence of risk). This design builds upon and extends the well-known Holt and Laury (Reference Holt and Laury2002, hereinafter HL) procedure for risk preference, by transposing that design from state-payoff space into time-dated payoffs. The HL task is popular in its own right as means of eliciting the curvature of utility under risk, and also forms the basis for the curvature adjustment in the joint estimation approach. Second, I examine the effect upon estimated discount rates of alternative measurements of utility—namely whether utility is assumed to be linear, inferred from risk preferences, or revealed through choices over time.

Several related studies have likewise sought to measure the curvature of utility directly from choices over time.Footnote 2 In common with this paper, these studies share the key insight that to identify the curvature of instantaneous utility it is necessary to construct choices involving bundles of time-dated payoffs, as opposed to boundary choices between all-sooner versus all-later payoffs.Footnote 3 These studies find, again in common with this paper, that instantaneous utility is significantly concave yet close to linear. In the following paragraphs, I discuss these studies, and explain how this paper differs from each of them.

Abdellaoui et al. (Reference Abdellaoui, Bleichrodt, l’Haridon and Paraschiv2013) compare the curvature of utilities elicited under risk and over time, however they are not concerned with implications for the estimation of discount rates. For risk, they elicit the certainty equivalent (CE) of a risky prospect that pays x with probability p or otherwise y. For time, they elicit the present equivalent (PE) of a temporal prospect that pays x at time k and y today. Thus notice that these two procedures are not exactly comparable. For risk, the CE is an amount paid in both states. This implies, firstly, that the impact of diminishing marginal utility upon the marginal rate of substitution vanishes at the CE (see Eq. 2 in Sect. 2.1), and secondly that the CE lies between x and y. By contrast for time, the PE is an amount paid solely on a single date. The impact of diminishing marginal utility is thus maximized because the difference in payoffs between the two dates is also maximal (as the payoff on the second date, k, is implicitly zero), and the PE may be larger than both x and y. Thus Abdellaoui et al. measure the curvature of utility over different intervals of payoffs for risk and time, and in such a way that diminishing marginal utility has differing effects upon the trade-offs faced in the two domains. The design of the experiment in this paper seeks to avoid these confounds.

Andreoni and Sprenger (Reference Andreoni and Sprenger2012a) and Andreoni et al. (Reference Andreoni, Kuhn and Sprenger2015) compare estimates of utility curvature and discounting elicited using the Convex Time Budget (CTB) procedure to measures derived using the binary choice methodology of Andersen et al. (Reference Andersen, Harrison, Lau and Rutström2008). The CTB design of Andreoni and Sprenger (Reference Andreoni and Sprenger2012a) identifies instantaneous utility by allowing subjects to choose any convex combination between an all-sooner and an all-later extreme, while the modified CTB of Andreoni et al. (Reference Andreoni, Kuhn and Sprenger2015) simplifies this to a multinomial choice. In this environment, the preference to smooth payoffs over time is expressed through the choice of an interior allocation. In fact, when payments on both dates are sent with certainty, choices occur predominantly at the corners of the budget set, indicating that utility is close to linear.Footnote 4 Andreoni and Sprenger (Reference Andreoni and Sprenger2012a) and Andreoni et al. (Reference Andreoni, Kuhn and Sprenger2015) compare this finding to that of a binary choice risk task of the type used by Andersen et al. (Reference Andersen, Harrison, Lau and Rutström2008). They find that the latter indicates substantially greater utility curvature, and that the two curvature measures are uncorrelated at an individual level. Andreoni et al. (Reference Andreoni, Kuhn and Sprenger2015) further show that the risk-elicited curvature measure overstates the preference for interior allocations in the modified CTB.

Thus, Andreoni and Sprenger (Reference Andreoni and Sprenger2012a) and Andreoni et al. (Reference Andreoni, Kuhn and Sprenger2015) compare utilities for risk and time elicited using different experimental designs (binary choice for risk and CTB for time), with different associated estimation procedures. However, it is well-known that owing to violations of procedure invariance, risk and time preferences may not be stable across elicitation procedures (e.g., Tversky et al. Reference Tversky, Slovic and Kahneman1990; Loomes and Pogrebna Reference Loomes and Pogrebna2014; Freeman et al. Reference Freeman, Manzini, Mariotti and Mittone2016). Moreover, the bulk of previous research on time preference uses binary choices, and estimation techniques for such data are well established in both the risk and time preference literatures. Estimation methodology for continuous and multinomial CTB data is less settled (see discussions in Andreoni and Sprenger Reference Andreoni and Sprenger2012a; Harrison et al. Reference Harrison, Lau and Rutström2013; Andreoni et al. Reference Andreoni, Kuhn and Sprenger2015). Thus, inferences from binary choice data for risk and CTB data for time may differ through any combination of: differences in experimental design, differences in estimation procedures,Footnote 5 or genuine differences in the curvatures of Bernoulli and instantaneous utility.

I seek to avoid these confounds by comparing the curvatures of utility for risk and time within a unified design and estimation framework, using binary choices for both. Moreover, my binary choice task for time is derived from a transposition of the standard HL task for risk: rather than varying probabilities (holding payoffs fixed), it is a payment date that varies instead. This ensures that when comparing these results to the risk preference task (or a joint estimation procedure as in Andersen et al. Reference Andersen, Harrison, Lau and Rutström2008), the estimation apparatus remains unchanged and it is only the source of information on the curvature of utility that differs.

The remainder of the paper proceeds as follows. Section 2 first interprets the HL design for risk in a state-preference framework before showing how it can be translated into time-dated payoffs and extended to identify both utility and discounting. The full experiment design consists of a series of choice lists that differ in whether the smaller-sooner option offers a more or less temporally-balanced combination of payoffs. If instantaneous utility is linear, a subject will have the same switch point in all lists, identifying the discount rate. However if utility is concave, this generates a preference for more temporally-balanced payoff bundles, resulting in systematic shifts in switching behavior across lists. Section 3 presents the results. The pattern implied by concave instantaneous utility is indeed observed, and is highly significant, but the magnitude is not large. The curvature of utility estimated from these choices is significantly concave, but less so than utility under risk, with the CRRA coefficient being an order of magnitude smaller. Adjusting for this degree of curvature has only a modest effect upon estimated discount rates compared to assuming linear utility, and a much smaller effect than when utility is inferred from risk preference using joint estimation. At an individual level, the curvatures of Bernoulli and instantaneous utility are uncorrelated. Joint estimates that constrain them to be the same predict time preference choices poorly because they overstate the preference for temporally-balanced payoff bundles. Section 4 concludes.

2 Design

2.1 State-preference representation of the HL design for risk

The HL experiment consists of a set of choices between two alternatives, labeled Options A and B, and is customarily presented as a choice list. Each alternative is a risky prospect that pays a low prize

in the “bad” state, with probability

in the “bad” state, with probability

, or a high prize

, or a high prize

in the “good” state, with probability

in the “good” state, with probability

. Options A and B represent two distinct payoff vectors, and in a given row of the choice list the probability

. Options A and B represent two distinct payoff vectors, and in a given row of the choice list the probability

is the same for both alternatives. Moving down the rows of the list, the payoff vectors remain unchanged and it is only the probability

is the same for both alternatives. Moving down the rows of the list, the payoff vectors remain unchanged and it is only the probability

that varies.

that varies.

Figure 1 illustrates using the payoffs used in this paper. Option A is a lottery that pays $17 in the bad state (plotted on the horizontal axis), and $20 in the good state (on the vertical).Footnote 6 Option B pays $1 in the bad state, and $38 in the good state.Footnote 7 Option A is safer in that the difference in payoffs

is relatively small, whereas Option B is risky in comparison; in Fig. 1, this is represented by the fact that Option A lies closer to the diagonal, whereas Option B is close to the axis. In keeping with the original HL design, the probability

is relatively small, whereas Option B is risky in comparison; in Fig. 1, this is represented by the fact that Option A lies closer to the diagonal, whereas Option B is close to the axis. In keeping with the original HL design, the probability

starts at 0.1 in the first row, and increases in increments of 0.1 up to a value of 1.0 in the final row.Footnote 8 The expected value of Option B thus increases more rapidly than that of Option A, and in the final row Option A is a dominated choice.

starts at 0.1 in the first row, and increases in increments of 0.1 up to a value of 1.0 in the final row.Footnote 8 The expected value of Option B thus increases more rapidly than that of Option A, and in the final row Option A is a dominated choice.

Fig. 1 State-preference representation of the HL design for risk

The rank-dependent utility of a risky prospect that pays

with probability

with probability

and

and

otherwise is:

otherwise is:

where

is the probability weighting function, and

is the probability weighting function, and

is the Bernoulli utility function. The (absolute) slope of an indifference curve is thus:

is the Bernoulli utility function. The (absolute) slope of an indifference curve is thus:

This slope is a product of two terms:

is the probability-weighted odds of the bad state, while the ratio of marginal utilities

is the probability-weighted odds of the bad state, while the ratio of marginal utilities

captures the preference to smooth payoffs over the good and bad states of nature.

captures the preference to smooth payoffs over the good and bad states of nature.

For the benchmark case of expected utility with a linear utility function,

and

and

, the slope reduces to the objective odds

, the slope reduces to the objective odds

and the indifference curves are linear. In the early rows of the choice list

and the indifference curves are linear. In the early rows of the choice list

is small and the indifference curves steeper than the chord AB, such that a risk-neutral subject prefers Option A. Moving down the rows of the list, as

is small and the indifference curves steeper than the chord AB, such that a risk-neutral subject prefers Option A. Moving down the rows of the list, as

increases the indifference curves become flatter, and the subject eventually switches to Option B. In particular, a risk-neutral subject chooses Option A in the first four rows, and Option B thereafter.Footnote 9

increases the indifference curves become flatter, and the subject eventually switches to Option B. In particular, a risk-neutral subject chooses Option A in the first four rows, and Option B thereafter.Footnote 9

Relative to this benchmark, a risk-averse subject continues to choose Option A at higher probabilities of the good state

. This may occur as the subject over-weights the odds of the bad state,Footnote 10 such that

. This may occur as the subject over-weights the odds of the bad state,Footnote 10 such that

and/or as Bernoulli utility is concave, such that

and/or as Bernoulli utility is concave, such that

. The impact of diminishing marginal utility vanishes when

. The impact of diminishing marginal utility vanishes when

, while it increases as the difference in payoffs grows. The indifference curves thus become steeper as they approach the vertical axis, such that the subject chooses Option A at larger values of

, while it increases as the difference in payoffs grows. The indifference curves thus become steeper as they approach the vertical axis, such that the subject chooses Option A at larger values of

owing to a preference to avoid unequal payoffs across states.

owing to a preference to avoid unequal payoffs across states.

2.2 Time-dated translation of the HL design for time

To translate the logic of the HL procedure into the domain of time preference, Options A and B are recast as temporal prospects that pay an amount

on a “sooner” date t, and an additional amount

on a “sooner” date t, and an additional amount

on a “later” date

on a “later” date

. Letting the date of the experiment be 0, t is the “front-end delay” to the sooner payment, while k is the “back-end delay” between the sooner and later payments. Throughout this paper, t and k are expressed in weeks, while interest and discount rates are expressed in annualized terms. Consistent with the HL procedure for risk, each set of choices is presented as a choice list. Within a given list, Options A and B represent two distinct payoff vectors, and in a given row the payment dates are the same for both alternatives. Moving down the rows of the list, the payoff vectors remain unchanged and it is only the payment dates, and specifically only the back-end delay k, that varies.

. Letting the date of the experiment be 0, t is the “front-end delay” to the sooner payment, while k is the “back-end delay” between the sooner and later payments. Throughout this paper, t and k are expressed in weeks, while interest and discount rates are expressed in annualized terms. Consistent with the HL procedure for risk, each set of choices is presented as a choice list. Within a given list, Options A and B represent two distinct payoff vectors, and in a given row the payment dates are the same for both alternatives. Moving down the rows of the list, the payoff vectors remain unchanged and it is only the payment dates, and specifically only the back-end delay k, that varies.

Figure 2 presents the format of the choice list for the pair of payoff vectors corresponding to the risk preference task described in Sect. 2.1. In the first row, Option A offers $17 in 1 week and $20 in 28 weeks, while Option B offers $1 in 1 week and $38 in 28 weeks. Thus Option A is “smaller-sooner” in that it offers a smaller total payment in undiscounted terms, but more on the sooner date, while Option B is “larger-later”. The front-end delay t is constant and equal to 1 week for all choices. The back-end delay k starts at 27 weeks in the first row and falls in decrements of 3 weeks down to 0 weeks in the final row. Thus in the final row all payments accrue after 1 week, such that Option A is a dominated choice.

Fig. 2 Sample choice list instrument for time preference elicitation

By choosing Option B in a given row, a subject forgoes

from the sooner payment and in exchange receives an additional

from the sooner payment and in exchange receives an additional

in the later payment, a return of 12.5%. Since the subject must wait k weeks to attain this return, the implied annual interest rate is

in the later payment, a return of 12.5%. Since the subject must wait k weeks to attain this return, the implied annual interest rate is

. As k falls, the subject waits a shorter length of time to realize the same return, and so the annual interest rate increases.Footnote 11

. As k falls, the subject waits a shorter length of time to realize the same return, and so the annual interest rate increases.Footnote 11

Relative to a more conventional time preference choice list, this design differs in two key respects. First, all choices involve bundles of payments on two dates, as opposed to either the sooner or later date. Second, variation in the interest rate is generated by varying payment dates while holding the payoffs constant, rather than the other way around. As I explain next, this makes it possible to vary interest rates orthogonally to implications for intertemporal substitution, i.e. whether it is the sooner, later, or neither option that offers a more temporally-balanced bundle of payoffs.

2.3 Disentangling utility curvature and time discounting

The discounted utility of a temporal prospect that pays

on date t and

on date t and

on date

on date

is:

is:

where

is the discount function, and

is the discount function, and

is the instantaneous utility function.Footnote 12 The (absolute) slope of an indifference curve is thus:

is the instantaneous utility function.Footnote 12 The (absolute) slope of an indifference curve is thus:

This slope is again a product of two terms:

is the relative value of utility at date t compared to

is the relative value of utility at date t compared to

, while

, while

captures the preference to smooth payoffs over time.

captures the preference to smooth payoffs over time.

For the benchmark case of exponential discounting with linear instantaneous utility,

(where

(where

is the annual discount rate) and

is the annual discount rate) and

, the slope reduces to

, the slope reduces to

and the indifference curves are linear. In early rows of the choice list, k is large and the indifference curves relatively steep, so a subject for whom

and the indifference curves are linear. In early rows of the choice list, k is large and the indifference curves relatively steep, so a subject for whom

is sufficiently large initially prefers Option A. Moving down the list, as k decreases the indifference curves become flatter, and the subject eventually switches to Option B. In particular, the subject chooses Option A as

is sufficiently large initially prefers Option A. Moving down the list, as k decreases the indifference curves become flatter, and the subject eventually switches to Option B. In particular, the subject chooses Option A as

, i.e. as

, i.e. as

, and Option B otherwise.

, and Option B otherwise.

Thus in the benchmark case, this design functions exactly as a conventional time preference choice list, in that the “switch point” from smaller-sooner to larger-later identifies bounds on the discount rate. Therefore, in contrast to the benchmark case for risk, there is no point prediction for the number of sooner choices. This simply reflects the fact that the discount rate

is an additional preference parameter that must be estimated, whereas in the case of risk the odds are objectively determined by the experimenter.

is an additional preference parameter that must be estimated, whereas in the case of risk the odds are objectively determined by the experimenter.

For the more general case of non-linear instantaneous utility, it follows that it will not be possible to also identify the curvature of utility from a single choice list. Figure 3 depicts indifference curves for two subjects who both prefer Option A in a given row of the list. The first, represented by the linear indifference curve, prefers Option A on account of impatience, i.e.

. The second, represented by the convex indifference curve, is relatively patient, i.e.

. The second, represented by the convex indifference curve, is relatively patient, i.e.

,Footnote 13 but has concave instantaneous utility (such that

,Footnote 13 but has concave instantaneous utility (such that

for

for

) and prefers A because it offers a more temporally-balanced stream of payoffs. Clearly, it is not possible to distinguish these cases simply by observing the switch point in a single choice list.

) and prefers A because it offers a more temporally-balanced stream of payoffs. Clearly, it is not possible to distinguish these cases simply by observing the switch point in a single choice list.

Fig. 3 Time-dated payoff representation of the HL design for time

Figure 3 also suggests two strategies by which it may be possible to distinguish between the cases. First, suppose subjects also face choices between A and C, where C is the payoff vector

. Relative to A, where B represents a deferral of payment, C represents expediting of payment at the same interest rate of 12.5% over k weeks. Then at the same row of an analogously-constructed CA choice list, the impatient subject with linear utility prefers C. On the other hand, the patient subject with concave utility continues to prefer A, both on account of the return for delay (discounting) and because A offers a more temporally-balanced stream of payoffs (utility). Second, consider choices between A and the payoff vector

. Relative to A, where B represents a deferral of payment, C represents expediting of payment at the same interest rate of 12.5% over k weeks. Then at the same row of an analogously-constructed CA choice list, the impatient subject with linear utility prefers C. On the other hand, the patient subject with concave utility continues to prefer A, both on account of the return for delay (discounting) and because A offers a more temporally-balanced stream of payoffs (utility). Second, consider choices between A and the payoff vector

, which is the midpoint of AB. Relative to A, B’ again represents deferral of payment, however the amount being deferred is smaller such that B’ is less unbalanced than B. At the same row of an AB’ choice list, the impatient subject with linear utility continues to prefer A. However the patient subject with concave utility may choose B’, but not B, if willing to save a smaller, but not a larger, amount.

, which is the midpoint of AB. Relative to A, B’ again represents deferral of payment, however the amount being deferred is smaller such that B’ is less unbalanced than B. At the same row of an AB’ choice list, the impatient subject with linear utility continues to prefer A. However the patient subject with concave utility may choose B’, but not B, if willing to save a smaller, but not a larger, amount.

2.4 Full design

The full design involves the five payoff vectors depicted in Fig. 3:

,

,

,

,

,

,

, and

, and

. Of these, C is “smallest-soonest”, while B is “largest-latest”. By construction, for any two vectors, the return for choosing the larger-later one is 12.5% over k weeks. Each subject completed six time preference choice lists, each in the format shown in Fig. 2, using the following pairs of payoff vectors: CA, C’A, AB’, AB, CB, and C’B’.Footnote 14 In each list, the smaller-sooner option was shown on the left as Option A, while the larger-later one was shown on the right as Option B—thus the alternatives were not identified as C, B’, etc. in materials presented to subjects. The front-end delay t was always one week, and the back-end delay k declined from 27 down to 0 weeks in each choice list, generating annual interest rates that increase from 25.46% up to infinity (in the final dominated choice).Footnote 15

. Of these, C is “smallest-soonest”, while B is “largest-latest”. By construction, for any two vectors, the return for choosing the larger-later one is 12.5% over k weeks. Each subject completed six time preference choice lists, each in the format shown in Fig. 2, using the following pairs of payoff vectors: CA, C’A, AB’, AB, CB, and C’B’.Footnote 14 In each list, the smaller-sooner option was shown on the left as Option A, while the larger-later one was shown on the right as Option B—thus the alternatives were not identified as C, B’, etc. in materials presented to subjects. The front-end delay t was always one week, and the back-end delay k declined from 27 down to 0 weeks in each choice list, generating annual interest rates that increase from 25.46% up to infinity (in the final dominated choice).Footnote 15

Because this design varies interest rates orthogonally to how near or far the payoff vectors are from the diagonal in Fig. 3, it is possible to identify both the discount rate and curvature of instantaneous utility directly from choices over time—without relying on a separate risk preference task or assuming that utility is the same for both risk and time.

Since by design the interest rate is the same at the corresponding row of each choice list, a subject with linear utility will have the same switch point in each. This is the analog to the point prediction that a risk-neutral subject makes four safe lottery choices in the risk task. On the other hand, a subject with concave instantaneous utility prefers to smooth payoffs over time. This subject will have a later switch point in the AB and AB’ choice lists, in which the smaller-sooner option is more temporally-balanced, than in the CA and C’A lists, in which it is the larger-later option that is more balanced. Details of this prediction are set out in Appendix A.1. It should be emphasized that this prediction holds regardless of the shape of the discount function, and does not rely upon exponential discounting.

In addition to the six time preference choice lists, each subject also completed a single risk preference choice list, using the classic AB parameter set described in Sect. 2.1. This makes it possible to compare the curvature of utility elicited under risk and over time, in a within-subjects design.

Two limitations of the design may be acknowledged. First, the annual interest rates offered in the experiment are rather high,Footnote 16 as it was not possible to extend k beyond six months since the last payment date fell shortly before the start of summer vacation.Footnote 17 Second, as all choice lists have the same front-end delay of one week, it is not possible to identify parameters of a non-exponential discount function. Rather, it is only possible to estimate an exponential discount rate (which may also be interpreted as the exponential component of a quasi-hyperbolic model). This design choice was made because the focus of this paper is to examine implications of concave instantaneous utility that do not depend on the shape of the discount function.

2.5 Procedures

A total of 122 student subjects participated in the experiment at the research laboratory of the School of Economics at The University of Sydney between 6 and 13 May 2014. The mean age of subjects was 20.4 years, and 55.7% were males. Subjects were recruited using ORSEE (Greiner Reference Greiner2015). To ensure that subjects would still be at university when payments were sent, students already in their final semester of study were not eligible to participate. Each session ran for approximately 75 minutes including instruction and payment, and the average payment was $45.2 (approximately USD 42.0 or EUR 28.5), inclusive of a $10 show-up fee. A total of 12 sessions were conducted, and the order of presentation of time preference choice lists was varied between sessions.Footnote 18 Each choice list consisted of ten decisions, so each subject made 70 choices in total. The experiment was conducted by pen-and-paper.

At the end of the session, one decision was drawn randomly and independently for each subject, and they were paid according to the choice made in that decision. Following the procedure of Andreoni and Sprenger (Reference Andreoni and Sprenger2012a), the $10 show-up fee was split into two equal installments of $5 paid by check on the sooner and later payment dates of the decision selected to count for payment. The payments chosen by the subject were added to these checks. Since the subject would in any case have to bank two checks, this ensured that there was no convenience benefit from choosing a more unbalanced payoff vector in order to amass payment on a single date. If one of the ten risk preference decisions was selected to count for payment, the realization of the chosen lottery was paid in cash at the end of the session, however the show-up fee was still paid in two checks of $5, sent one and sixteen weeks after the experiment. This ensured that any wealth effect attributable to the show-up fee would be the same for both risk and time preference decisions.Footnote 19

The procedures also incorporated several measures introduced by Andreoni and Sprenger (Reference Andreoni and Sprenger2012a), as adapted by Cheung (Reference Cheung2015), to enhance the credibility of payment and minimize the background risk of receiving payment in the future. First, all checks were drawn on the campus branch of the National Australia Bank and mailed by Australia Post guaranteed Express Post. Australia Post guarantees next-day delivery for articles mailed by Express Post, at a cost of $6 per envelope. Since every subject addressed their own envelopes prior to making their choices, they could observe that the experimenter was willing to pay $6 to mail a check to the value of as little as $5 by Express Post. This imparted a high level of credibility to the payments.Footnote 20 At the end of the session, each subject wrote their own payment amounts and dates on the inside of each envelope, and was given a copy of the receipt form showing these amounts and dates, as well as the business card of the experimenter to contact in the event of a payment not arriving as expected.

3 Results

Section 3.1 describes aggregate behavior in the risk and time preference tasks, before Sects. 3.2 and 3.3 report structural estimates of utility and discount functions for a representative agent. The key findings are that instantaneous utility is significantly concave, but less so than Bernoulli utility for risk, and the effect of correcting for the curvature of instantaneous utility upon the discount rate is modest. Section 3.4 considers joint estimation, which has a more pronounced effect, while Sect. 3.5 introduces an alternative to discounted utility that is compatible with more substantial utility curvature. Section 3.6 reports a number of robustness checks to the representative agent estimates. Section 3.7 turns to estimation and prediction at an individual level. It shows that the curvatures of Bernoulli and instantaneous utility are not significantly correlated, and individual estimates that infer the curvature of utility from choices over time predict subjects’ time preference choices better than linear utility, while joint estimates do not.

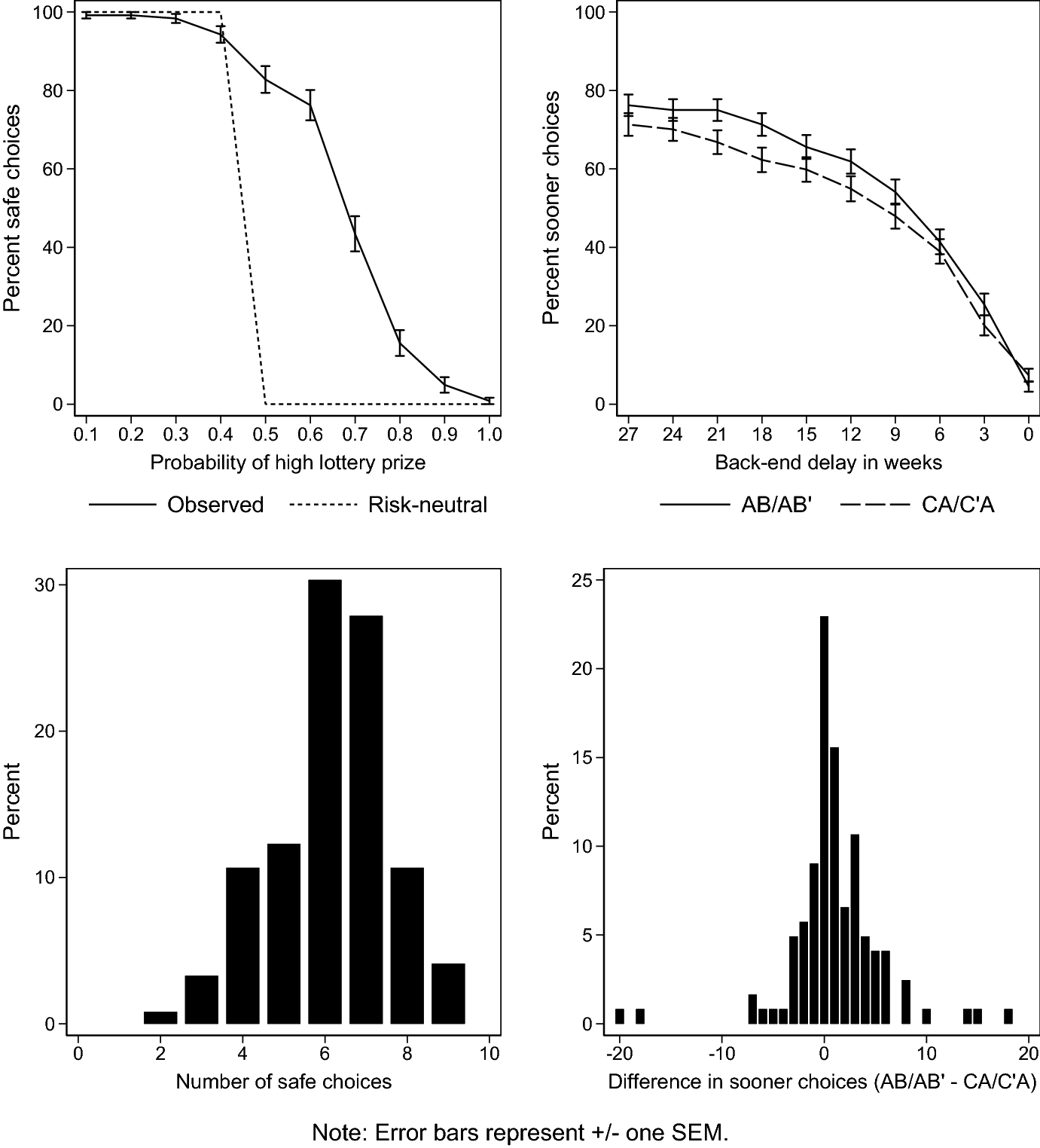

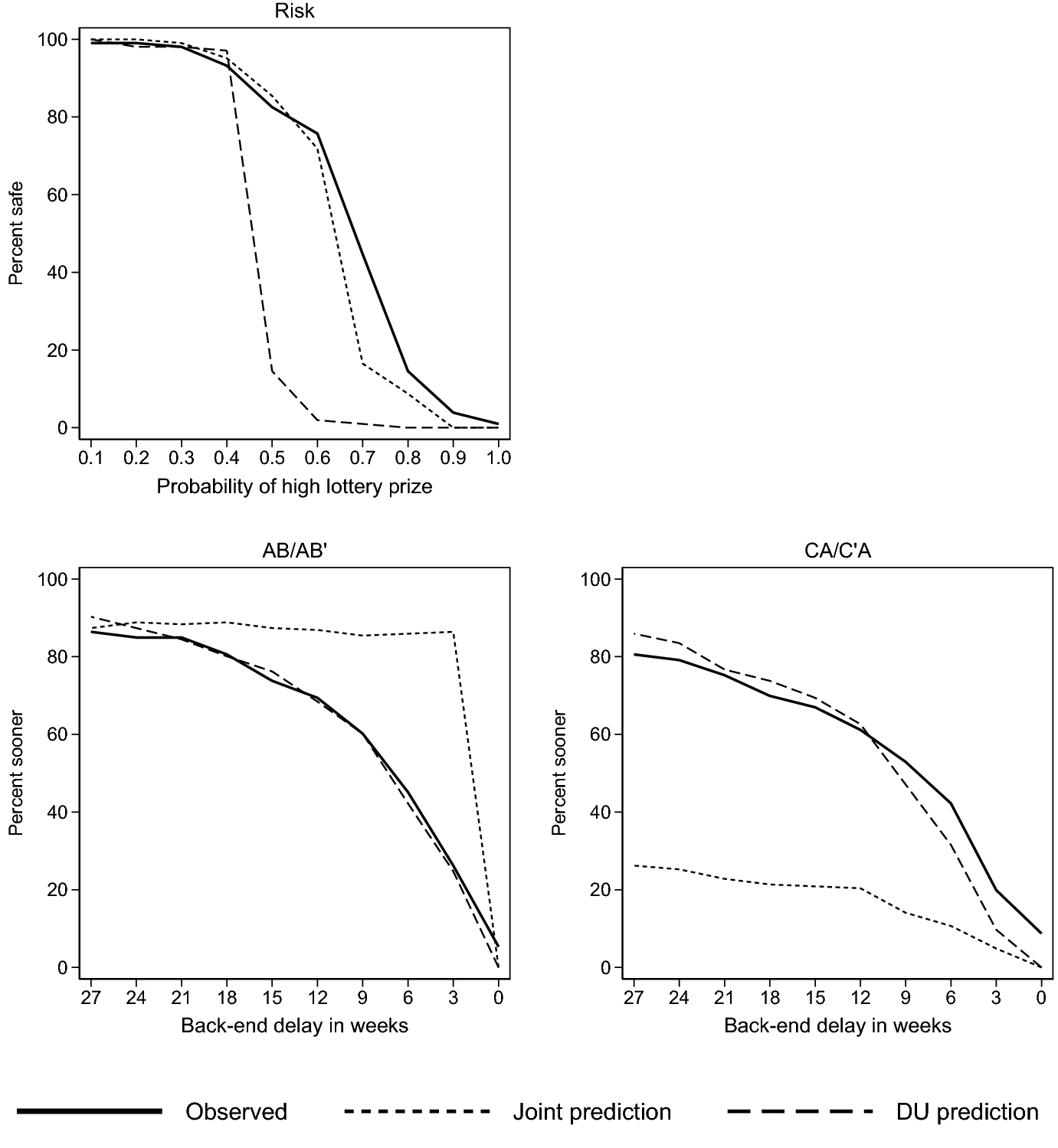

3.1 Descriptive analysis

Figure 4 summarizes aggregate choice behavior in the experiment. The upper left panel reports the percentage of subjects who choose the safer Option A for each row of the risk preference task. The dashed line depicts the benchmark prediction under risk neutrality, the solid line depicts observed choices, and error bars represent ± one standard error of the mean for a binomial proportion. The lower left panel reports a histogram of the number of safe choices made by each subject. The median subject makes six such choices, and the number of safe choices differs significantly from the risk-neutral benchmark of four, with

in both a sign test and a Wilcoxon signed-ranks test (all tests reported throughout the paper are two-sided).Footnote 21

in both a sign test and a Wilcoxon signed-ranks test (all tests reported throughout the paper are two-sided).Footnote 21

Fig. 4 Choice behavior in risk and time preference tasks

Turning to behavior in time preference tasks, the upper right panel reports the percentage of smaller-sooner choices as a function of the back-end delay, separately for the pooled AB/AB’ and CA/C’A choice lists. Appendix B.1 reports separate figures for each list. The proportion of sooner choices declines smoothly as the back-end delay falls and the interest rate increases, suggesting that subjects understood the underlying trade-off entailed in waiting a longer or shorter time for a given-sized increase in undiscounted payoffs.

Under linear utility subjects are predicted to make the same choices in all lists, while departures from linearity are expressed as differences across lists. In particular, a subject with concave utility prefers to smooth payoffs over time, and thus makes more sooner choices in AB/AB’ choice lists (in which the smaller-sooner option is more temporally balanced) than in CA/C’A lists (in which the larger-later option is more balanced). The upper right panel of Fig. 4 confirms a small, but clearly discernible shift in the direction predicted by concave utility. At every back-end delay except zero (where the sooner option is dominated), subjects make more sooner choices in AB/AB’ than in CA/C’A. To illustrate the magnitude of these differences, the error bars represent ± one standard error of the mean for a binomial proportion.

The lower right panel of Fig. 4 reports a histogram of the difference in the number of sooner choices made by each subject between the AB/AB’ and CA/C’A choice lists. The mode of this distribution is at zero, corresponding to linear utility, but there is greater mass to the right indicating a tendency toward concavity. The median subject makes a total of 13 sooner choices in the combined AB/AB’ choice lists, compared to 11.5 in the CA/C’A lists. This difference is highly significant, with

in a sign test, or

in a sign test, or

in a Wilcoxon signed-ranks test.Footnote 22 This evidence of a systematic tendency to prefer the more balanced payoff vector A, consistent with a preference to smooth payoffs over time, does not rely on any assumptions on the functional form of utility.Footnote 23

in a Wilcoxon signed-ranks test.Footnote 22 This evidence of a systematic tendency to prefer the more balanced payoff vector A, consistent with a preference to smooth payoffs over time, does not rely on any assumptions on the functional form of utility.Footnote 23

Figure 4 establishes that, in both risk and time preference, there is clear evidence of the choice patterns implied by concave utility. The finding for risk replicates other studies that use the HL design, while the finding for time is a novel result of transposing that design into the domain of time preference. Moreover, while both effects are highly significant, it is clear that the magnitude is smaller in choice over time. This suggests that while instantaneous utility for time is indeed concave, it may be less concave than Bernoulli utility for risk. To formalize this observation, I next estimate structural preference models for a representative agent, building upon well-established procedures documented by Harrison and Rutström (Reference Harrison, Rutström, Cox and Harrison2008) for risk and Andersen et al. (Reference Andersen, Harrison, Lau and Rutström2008, Reference Andersen, Harrison, Lau and Rutström2014) for time.

3.2 Utility curvature under risk

For risk preference, I assume a constant relative risk aversion (CRRA) functional form for Bernoulli utility:

such that

corresponds to linear utility, while

corresponds to linear utility, while

implies concave utility. I begin with expected utility, but the exposition treats this as the special case of rank-dependent utility with

implies concave utility. I begin with expected utility, but the exposition treats this as the special case of rank-dependent utility with

. Given some candidate value of

. Given some candidate value of

(and probability weighting parameters), the rank-dependent utility of each lottery is evaluated. Then, adopting a “contextual” error specification (Wilcox Reference Wilcox2011), the probability that Option B is chosen is modeled as:

(and probability weighting parameters), the rank-dependent utility of each lottery is evaluated. Then, adopting a “contextual” error specification (Wilcox Reference Wilcox2011), the probability that Option B is chosen is modeled as:

where

is the cumulative logistic distribution function,

is the cumulative logistic distribution function,

is the difference between the maximum and minimum utilities over all prizes in the choice set,Footnote 24 and

is the difference between the maximum and minimum utilities over all prizes in the choice set,Footnote 24 and

is a structural “noise” parameter for the risk preference choices. As

is a structural “noise” parameter for the risk preference choices. As

goes to zero, the lottery with the larger RDU is chosen deterministically, while as

goes to zero, the lottery with the larger RDU is chosen deterministically, while as

goes to infinity, the choice probability goes to one-half such that choices are essentially random. The data consists of 1220 observations, being ten binary choices in the risk preference task for each of 122 subjects. The parameters are estimated to maximize the likelihood of the observed choices using Stata 16, with robust standard errors clustered at the level of individual subjects.

goes to infinity, the choice probability goes to one-half such that choices are essentially random. The data consists of 1220 observations, being ten binary choices in the risk preference task for each of 122 subjects. The parameters are estimated to maximize the likelihood of the observed choices using Stata 16, with robust standard errors clustered at the level of individual subjects.

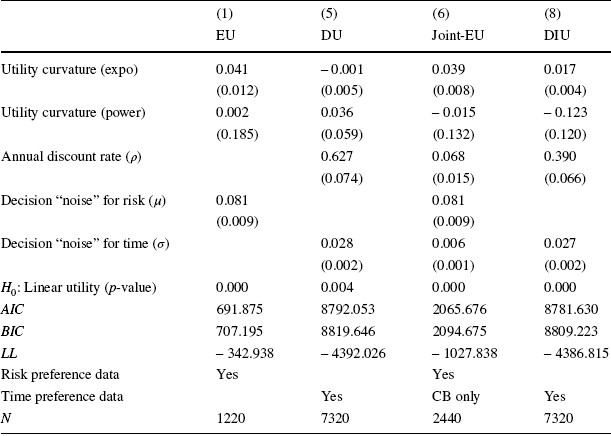

Model (1) in Table 1 reports estimates under expected utility. The point estimate of

is 0.547, with a standard error of 0.036. This implies substantial concavity of Bernoulli utility, and sits comfortably within the range of previously-reported estimates using similar experimental designs and estimation procedures.Footnote 25

is 0.547, with a standard error of 0.036. This implies substantial concavity of Bernoulli utility, and sits comfortably within the range of previously-reported estimates using similar experimental designs and estimation procedures.Footnote 25

Table 1 Representative agent estimates of utility curvature and discount rates

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

|

|---|---|---|---|---|---|---|---|---|

|

EU |

RDU |

Linear |

Linear-CB |

DU |

Joint-EU |

Joint-RDU |

DIU |

|

|

CRRA utility curvature (

|

0.547 |

0.206 |

0.018 |

0.456 |

0.421 |

0.226 |

||

|

(0.036) |

(0.095) |

(0.006) |

(0.012) |

(0.020) |

(0.060) |

|||

|

Probability weighting (

|

0.788 |

0.789 |

||||||

|

(0.280) |

(0.052) |

|||||||

|

Annual discount rate (

|

0.639 |

0.622 |

0.626 |

0.065 |

0.107 |

0.504 |

||

|

(0.077) |

(0.075) |

(0.074) |

(0.017) |

(0.025) |

(0.063) |

|||

|

Decision “noise” for risk (

|

0.082 |

0.088 |

0.083 |

0.073 |

||||

|

(0.009) |

(0.009) |

(0.008) |

(0.009) |

|||||

|

Decision “noise” for time (

|

0.028 |

0.034 |

0.028 |

0.006 |

0.009 |

0.027 |

||

|

(0.002) |

(0.003) |

(0.002) |

(0.002) |

(0.002) |

(0.002) |

|||

|

AIC |

689.875 |

685.734 |

8807.895 |

1412.456 |

8790.165 |

2082.889 |

2061.119 |

8785.710 |

|

BIC |

700.089 |

701.054 |

8821.692 |

1422.670 |

8810.860 |

2106.088 |

2090.117 |

8806.405 |

|

LL |

– 342.938 |

– 339.867 |

– 4401.948 |

– 704.228 |

– 4392.083 |

– 1037.445 |

– 1025.559 |

– 4389.855 |

|

Probability weighting function |

Gul |

Prelec-I |

||||||

|

Risk preference data |

Yes |

Yes |

Yes |

Yes |

||||

|

Time preference data |

Yes |

CB only |

Yes |

CB only |

CB only |

Yes |

||

|

N |

1220 |

1220 |

7320 |

1220 |

7320 |

2440 |

2440 |

7320 |

Cluster robust standard errors in parentheses

As discussed in Sect. 2.1, risk aversion in HL-style tasks may be driven by curvature of the utility function, and/or by non-linear probability weighting. Therefore, just as assuming linear utility may cause estimates of the discount rate to be biased in choice over time, assuming linear probability weighting may cause estimates of the utility function to be biased in choice under risk. Indeed, Drichoutis and Lusk (Reference Drichoutis and Lusk2016) claim that risk aversion in HL tasks may be solely a product of probability weighting as opposed to utility curvature: in their estimates of a rank-dependent model they find significant non-linear probability weighting, while the CRRA coefficient does not differ significantly from zero. While this finding is arguably at odds with other existing literature,Footnote 26 it highlights the importance of allowing for probability weighting when comparing the curvature of utility elicited under risk and over time.

To examine the robustness of concave Bernoulli utility to the possibility of non-linear probability weighting, I estimate rank-dependent models for each parametric form of the probability weighting function in Section 3.6 of the survey by Fehr-Duda and Epper (Reference Fehr-Duda and Epper2012). The Bayesian information criterion (BIC) in fact selects the expected utility specification of model (1) in Table 1. The Akaike information criterion (AIC), which penalizes model complexity less severely than the BIC, selects a model with a single-parameter weighting function from the theory of disappointment aversion of Gul (Reference Gul1991):

. The resulting estimates are set out as model (2) in Table 1. This weighting function simplifies to linearity at

. The resulting estimates are set out as model (2) in Table 1. This weighting function simplifies to linearity at

, a restriction that is clearly rejected with

, a restriction that is clearly rejected with

. The implied weighting function is convex, and is depicted by the dashed line in Fig. 5. For the purpose of this paper, the effect on the estimate of utility curvature is of greatest interest. This estimate is now smaller (and less precisely estimated) than under expected utility. However, it will transpire that it is still considerably greater than the curvature of instantaneous utility estimated from choices over time.

. The implied weighting function is convex, and is depicted by the dashed line in Fig. 5. For the purpose of this paper, the effect on the estimate of utility curvature is of greatest interest. This estimate is now smaller (and less precisely estimated) than under expected utility. However, it will transpire that it is still considerably greater than the curvature of instantaneous utility estimated from choices over time.

Fig. 5 Estimated probability weighting functions

3.3 Utility curvature and discounting over time

I next set out how the data from the six time preference choice lists can be used to estimate both the curvature of instantaneous utility and the discount rate, adopting similar procedures to Sect. 3.2 and Andersen et al. (Reference Andersen, Harrison, Lau and Rutström2008, Reference Andersen, Harrison, Lau and Rutström2014). I assume a CRRA form for the instantaneous utility function:

and an exponential form for the discount function:

where

captures the curvature of instantaneous utility and

captures the curvature of instantaneous utility and

is the annual discount rate. Given candidate values of

is the annual discount rate. Given candidate values of

and

and

, the discounted utility of each alternative is evaluated and the probability that the alternative presented as Option B is chosen is modeled as:

, the discounted utility of each alternative is evaluated and the probability that the alternative presented as Option B is chosen is modeled as:

where

is a contextual normalization term,Footnote 27 and

is a contextual normalization term,Footnote 27 and

is a noise parameter for the time preference choices.

is a noise parameter for the time preference choices.

It is worth emphasizing that this framework is essentially the same as that of Andersen et al. (Reference Andersen, Harrison, Lau and Rutström2008, Reference Andersen, Harrison, Lau and Rutström2014), except that information on utility curvature is obtained directly from choices over time instead of a separate risk preference task, so it is not necessary to equate Bernoulli utility for risk with instantaneous utility for time. The data consists of 7320 observations, being ten binary choices in each of six time preference choice lists for each of 122 subjects. The parameters

,

,

, and

, and

are estimated by maximum likelihood in Stata 16, with robust standard errors clustered at the level of individual subjects.

are estimated by maximum likelihood in Stata 16, with robust standard errors clustered at the level of individual subjects.

Before turning to the full results, model (3) in Table 1 reports a linear utility specification, with

constrained to zero, giving an estimated annual discount rate of 63.9%. While this is higher than prevailing market interest rates, it is not extreme by the standards of the literature.Footnote 28 Model (4) reports a linear utility specification using only the data of the CB choice list in which the smaller-sooner option pays

constrained to zero, giving an estimated annual discount rate of 63.9%. While this is higher than prevailing market interest rates, it is not extreme by the standards of the literature.Footnote 28 Model (4) reports a linear utility specification using only the data of the CB choice list in which the smaller-sooner option pays

while larger-later pays

while larger-later pays

. This is included for comparability with more conventional designs that offer all-sooner or all-later payments, as well as the subsequent replication of joint estimation invoking utility from the risk preference task in Sect. 3.4. The resulting estimate of the discount rate is very close to that of model (3).

. This is included for comparability with more conventional designs that offer all-sooner or all-later payments, as well as the subsequent replication of joint estimation invoking utility from the risk preference task in Sect. 3.4. The resulting estimate of the discount rate is very close to that of model (3).

Model (5) reports the main discounted utility estimates, allowing non-linear instantaneous utility revealed through data on choices over time. In this model, the point estimate of

is 0.018 with a standard error of 0.006, indicating significantly concave utility. This is consistent with the model-free analysis in Sect. 3.1. However, the estimate of

is 0.018 with a standard error of 0.006, indicating significantly concave utility. This is consistent with the model-free analysis in Sect. 3.1. However, the estimate of

is an order of magnitude smaller than estimates of

is an order of magnitude smaller than estimates of

from risk preference data in models (1) and (2). Because the estimated curvature of instantaneous utility is modest, the effect of correcting for this concavity upon the discount rate is mild: the estimate of

from risk preference data in models (1) and (2). Because the estimated curvature of instantaneous utility is modest, the effect of correcting for this concavity upon the discount rate is mild: the estimate of

falls from 63.9% in model (3) to 62.6% in model (5). Both the AIC and BIC select the non-linear utility specification of model (5) over the more parsimonious linear utility specification in model (3).

falls from 63.9% in model (3) to 62.6% in model (5). Both the AIC and BIC select the non-linear utility specification of model (5) over the more parsimonious linear utility specification in model (3).

3.4 Joint estimation

The modest effect of correcting for the curvature of instantaneous utility may be contrasted with that of a joint estimation procedure that combines risk and time preference data and imposes a single utility function upon both. To illustrate, I pool the data of the risk task with that of the CB choice list, which is comparable to conventional time preference data in that the payoffs are essentially at the all-sooner or all-later corners. The probability of making a risky lottery choice is modeled by Eq. 6 while that of making a larger-later choice is modeled by Eq. 9. The noise terms

and

and

are allowed to differ across risk and time preference tasks, but the utility function is constrained to be the same for both, such that

are allowed to differ across risk and time preference tasks, but the utility function is constrained to be the same for both, such that

. The data consists of 2440 observations, being ten risk and ten time preference choices for each of 122 subjects, and the parameters are estimated to maximize the joint likelihood of both sets of choices.

. The data consists of 2440 observations, being ten risk and ten time preference choices for each of 122 subjects, and the parameters are estimated to maximize the joint likelihood of both sets of choices.

Model (6) in Table 1 reports joint estimates assuming expected utility for risk. The estimate of utility curvature is 0.456 with a standard error of 0.012, reflecting the influence of risk aversion in the lottery choices, while the estimated annual discount rate falls to 6.5%. This compares to an estimate of 62.2% in model (4), which uses the same CB time preference data but assumes linear utility.

To allow for non-linear probability weighting in the risk preference data, I again re-estimate the joint model assuming rank-dependent utility for each parametric weighting function in Fehr-Duda and Epper (Reference Fehr-Duda and Epper2012). The effect upon utility and discounting is very similar across all specifications: the estimate of utility curvature falls to between 0.419 and 0.427 while the estimated discount rate increases slightly to between 10.0 and 10.9%. Both the AIC and BIC select a specification with a single-parameter weighting function from Prelec (Reference Prelec1998):

, and the resulting estimates are reported as model (7) in Table 1. This weighting function simplifies to linearity at

, and the resulting estimates are reported as model (7) in Table 1. This weighting function simplifies to linearity at

, a restriction that is rejected with

, a restriction that is rejected with

in a Wald test. The implied weighting function is inverse-S shaped, and is depicted by the solid line in Fig. 5.

in a Wald test. The implied weighting function is inverse-S shaped, and is depicted by the solid line in Fig. 5.

For the purpose of this paper, the key conclusions are twofold. First, even allowing for probability weighting, joint estimates of utility curvature which impose the restriction that

are considerably larger than the discounted utility estimate in model (5) which imposes no such restriction. Second, relative to the linear utility benchmark of model (4), the effect upon the discount rate of correcting for this amount of curvature is dramatic. The discount rates in models (6) and (7) are substantially smaller than the lowest interest rate offered in the experiment, suggesting that joint estimation may have yielded an over-correction.

are considerably larger than the discounted utility estimate in model (5) which imposes no such restriction. Second, relative to the linear utility benchmark of model (4), the effect upon the discount rate of correcting for this amount of curvature is dramatic. The discount rates in models (6) and (7) are substantially smaller than the lowest interest rate offered in the experiment, suggesting that joint estimation may have yielded an over-correction.

3.5 Discounted incremental utility

In Sects. 3.3 and 3.4, and models (3) through (7) in Table 1, I explored the effect of alternative assumptions about the nature of instantaneous utility—whether it is taken to be linear as in models (3) and (4), revealed through responses to varying opportunities for intertemporal substitution as in model (5), or equated with Bernoulli utility for risk as in models (6) and (7). It was assumed throughout that the underlying framework to evaluate streams of payoffs over time is given by the discounted utility model in Eq. 3.

Blavatskyy (Reference Blavatskyy2016) has argued that discounted utility may give rise to violations of intertemporal monotonicity when utility is not linear. In particular, it is possible for discounted utility to increase when a payoff is split into two parts, one of which is slightly delayed. That is, if

is sufficiently concave while

is sufficiently concave while

is close to

is close to

it is possible to have:

it is possible to have:

This implies that there may be a benefit to delay without any compensating increase in the magnitude of the payoff. The issue occurs when the impact of diminishing marginal utility as a payoff is divided in two outweighs the impact of discounting as a portion of it is delayed. This may occur in any model that has the discounted utility structure of Eq. 3, and is not specific to any functional form of the discount function

such as exponential discounting. Assuming discounted utility, it can be avoided only if utility is linear. It thus represents a theoretical argument for why discounted utility may be incompatible with substantial non-linearity of instantaneous utility, as found empirically in model (5) of Table 1.

such as exponential discounting. Assuming discounted utility, it can be avoided only if utility is linear. It thus represents a theoretical argument for why discounted utility may be incompatible with substantial non-linearity of instantaneous utility, as found empirically in model (5) of Table 1.

The argument of Blavatskyy (Reference Blavatskyy2016) is analogous to how simple probability weighting may violate first-order stochastic dominance in the original prospect theory of Kahneman and Tversky (Reference Kahneman and Tversky1979). In that setting, the solution proposed by Quiggin (Reference Quiggin1982) is to construct decision weights from a transformation of the cumulative probabilities instead of directly transforming the probabilities themselves. In the context of time, the solution proposed by Blavatskyy (Reference Blavatskyy2016) is to apply a utility transformation to the cumulative payoffs instead of directly to the payoffs themselves. This gives rise to the model of discounted incremental utility (Blavatskyy Reference Blavatskyy2016, equation 3) which replaces discounted utility by:

This states that future payoffs are evaluated by the discounted value of their incremental contribution to the utility of the cumulated payoffs,

.

.

Estimation of the discounted incremental model requires data on choices over non-degenerate streams, such as that reported in this paper,Footnote 29 as opposed to conventional choices over all-sooner versus all-later payoffs which never cumulate. If the cumulative utility function is linear then Eq. 10, like Eq. 3, simplifies to discounted linear utility, in which case a subject is again predicted to have the same switch point in all six choice lists. However if the cumulative utility function is concave, I show in Appendix A.3 that discounted incremental utility again predicts a later switch point in AB/AB’ than in CA/C’A choice lists.

To estimate the model I again assume a CRRA form, this time for the utility of cumulated payoffs, X:

and the exponential discount function of Eq. 8, and define choice probabilities analogously to Eq. 9 except replacing DU by DIU. The model is estimated using the same set of 7320 observations from six time preference choice lists as used in models (3) and (5) of Table 1.

Estimates of the discounted incremental specification are reported as model (8) in Table 1. The curvature of cumulative utility is significantly concave, with a CRRA coefficient of 0.226 and standard error of 0.060. This is substantially larger than the estimated curvature of instantaneous utility in the discounted utility specification of model (5). Allowing for this amount of curvature reduces the estimate of the annual discount rate from 63.9% under linear utility in model (3) to 50.4% in model (8). The discounted incremental specification has the same number of parameters as the discounted utility model, and a superior log-likelihood. As a result, both the AIC and BIC select this model over both the discounted utility and linear models.

3.6 Robustness checks

In this section, I report several robustness checks of the key representative agent estimates to alternative structural assumptions. Table 2 reports expected utility, discounted utility, joint, and discounted incremental estimates assuming a constant absolute risk aversion form for utility:

. Table 3 reports corresponding estimates assuming expo-power utility (Saha Reference Saha1993; Holt and Laury Reference Holt and Laury2002):

. Table 3 reports corresponding estimates assuming expo-power utility (Saha Reference Saha1993; Holt and Laury Reference Holt and Laury2002):

. These analyses replicate all key implications of Table 1: instantaneous utility in model (5) is significantly concaveFootnote 30 though substantially less so than Bernoulli utility in model (1); the discount rate in model (5) is only marginally smaller than that assuming linear utility (c.f. Table 1, model (3)), whereas the one obtained from joint estimation in model (6) is substantially lower; and the effects of discounted incremental utility in model (8) are similar to those in Table 1.

. These analyses replicate all key implications of Table 1: instantaneous utility in model (5) is significantly concaveFootnote 30 though substantially less so than Bernoulli utility in model (1); the discount rate in model (5) is only marginally smaller than that assuming linear utility (c.f. Table 1, model (3)), whereas the one obtained from joint estimation in model (6) is substantially lower; and the effects of discounted incremental utility in model (8) are similar to those in Table 1.

Table 2 Representative agent estimates under CARA utility

|

(1) |

(5) |

(6) |

(8) |

|

|---|---|---|---|---|

|

EU |

DU |

Joint-EU |

DIU |

|

|

CARA utility curvature |

0.041 |

0.001 |

0.040 |

0.018 |

|

(0.003) |

(0.000) |

(0.002) |

(0.005) |

|

|

Annual discount rate (

|

0.624 |

0.068 |

0.424 |

|

|

(0.073) |

(0.016) |

(0.065) |

||

|

Decision “noise” for risk (

|

0.081 |

0.081 |

||

|

(0.009) |

(0.009) |

|||

|

Decision “noise” for time (

|

0.028 |

0.006 |

0.027 |

|

|

(0.002) |

(0.001) |

(0.002) |

||

|

AIC |

689.875 |

8790.505 |

2063.699 |

8780.517 |

|

BIC |

700.089 |

8811.200 |

2086.898 |

8801.212 |

|

LL |

– 342.938 |

– 4392.252 |

– 1027.849 |

– 4387.259 |

|

Risk preference data |

Yes |

Yes |

||

|

Time preference data |

Yes |

CB only |

Yes |

|

|

N |

1220 |

7320 |

2440 |

7320 |

Clustered standard errors in parentheses. Column numbers indicate corresponding models in Table 1

Table 3 Representative agent estimates under expo-power utility

|

(1) |

(5) |

(6) |

(8) |

|

|---|---|---|---|---|

|

EU |

DU |

Joint-EU |

DIU |

|

|

Utility curvature (expo) |

0.041 |

– 0.001 |

0.039 |

0.017 |

|

(0.012) |

(0.005) |

(0.008) |

(0.004) |

|

|

Utility curvature (power) |

0.002 |

0.036 |

– 0.015 |

– 0.123 |

|

(0.185) |

(0.059) |

(0.132) |

(0.120) |

|

|

Annual discount rate (

|

0.627 |

0.068 |

0.390 |

|

|

(0.074) |

(0.015) |

(0.066) |

||

|

Decision “noise” for risk (

|

0.081 |

0.081 |

||

|

(0.009) |

(0.009) |

|||

|

Decision “noise” for time (

|

0.028 |

0.006 |

0.027 |

|

|

(0.002) |

(0.001) |

(0.002) |

||

|

|

0.000 |

0.004 |

0.000 |

0.000 |

|

AIC |

691.875 |

8792.053 |

2065.676 |

8781.630 |

|

BIC |

707.195 |

8819.646 |

2094.675 |

8809.223 |

|

LL |

– 342.938 |

– 4392.026 |

– 1027.838 |

– 4386.815 |

|

Risk preference data |

Yes |

Yes |

||

|

Time preference data |

Yes |

CB only |

Yes |

|

|

N |

1220 |

7320 |

2440 |

7320 |

Clustered standard errors in parentheses. Column numbers indicate corresponding models in Table 1

Table 4 reports linear, discounted utility, joint, and discounted incremental estimates for CRRA utility using an alternative contextual normalization that replaces the expression in footnote 27 with

(see Blavatskyy and Maafi Reference Blavatskyy and Maafi2018, p. 278). That is, instead of normalizing by the difference in discounted utilities between the best and worst payoff streams, these estimates normalize by the difference in instantaneous utilities between the best and worst payoffs, which does not depend upon the discount function.Footnote 31 Again, all key implications of Table 1 are maintained.

(see Blavatskyy and Maafi Reference Blavatskyy and Maafi2018, p. 278). That is, instead of normalizing by the difference in discounted utilities between the best and worst payoff streams, these estimates normalize by the difference in instantaneous utilities between the best and worst payoffs, which does not depend upon the discount function.Footnote 31 Again, all key implications of Table 1 are maintained.

Table 4 Representative agent estimates under alternative contextual normalization

|

(3) |

(5) |

(6) |

(8) |

|

|---|---|---|---|---|

|

Linear |

DU |

Joint-EU |

DIU |

|

|

CRRA utility curvature |

0.018 |

0.455 |

0.180 |

|

|

(0.006) |

(0.012) |

(0.066) |

||

|

Annual discount rate (

|

0.662 |

0.648 |

0.066 |

0.543 |

|

(0.083) |

(0.080) |

(0.017) |

(0.076) |

|

|

Decision “noise” for risk (

|

0.083 |

|||

|

(0.008) |

||||

|

Decision “noise” for time (

|

0.053 |

0.052 |

0.012 |

0.046 |

|

(0.004) |

(0.004) |

(0.003) |

(0.004) |

|

|

AIC |

8771.565 |

8754.908 |

2082.580 |

8759.751 |

|

BIC |

8785.362 |

8775.603 |

2105.779 |

8780.446 |

|

LL |

– 4383.783 |

– 4374.454 |

– 1037.290 |

– 4376.875 |

|

Risk preference data |

Yes |

|||

|

Time preference data |

Yes |

Yes |

CB only |

Yes |

|

N |

7320 |

7320 |

2440 |

7320 |

Clustered standard errors in parentheses. Column numbers indicate corresponding models in Table 1

3.7 Individual estimation and prediction

In this section, I extend the analysis to estimation at an individual level, and examine the performance of individual estimates in predicting subjects’ choices in the risk and time preference decisions respectively.

In the full sample of 122 subjects there are fifteen who choose larger-later in all 60 time preference decisions, and four who choose smaller-sooner in all 54 decisions where it is not dominated. I thus focus on the remaining 103 subjects in individual estimation. Since there is only a single risk preference choice list, it is not possible to estimate probability weighting parameters at an individual level. I thus report individual estimates for five models: the expected utility specification in model (1) of Table 1, the linear utility specification in model (3), the discounted utility specification in model (5), the joint estimation specification in model (6), and the discounted incremental specification in model (8). Individual estimation was performed in Matlab R2018b, after first replicating the corresponding representative agent estimates from Table 1.

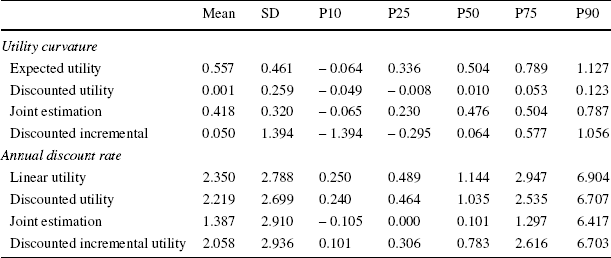

Table 5 reports summary statistics for four individual measures of CRRA utility curvature (not estimated under linear utility) and four individual estimates of the annual discount rate (not estimated under expected utility). Histograms for each set of estimates are reported in Appendix B.2. For utility curvature, the mean and median estimates under expected utility, discounted utility and joint estimation are very similar to the corresponding representative agent estimates. However for discounted incremental utility, the mean and median curvature are closer to linearity than the aggregate estimate, and the variance is considerable. For discounting, the mean and median estimates are consistently larger than the corresponding estimates in Table 1, in part reflecting the fact that the individual estimation sample excludes the fifteen most patient subjects.Footnote 32

Table 5 Summary statistics of individual utility curvature and discount rate estimates

|

Mean |

SD |

P10 |

P25 |

P50 |

P75 |

P90 |

|

|---|---|---|---|---|---|---|---|

|

Utility curvature |

|||||||

|

Expected utility |

0.557 |

0.461 |

– 0.064 |

0.336 |

0.504 |

0.789 |

1.127 |

|

Discounted utility |

0.001 |

0.259 |

– 0.049 |

– 0.008 |

0.010 |

0.053 |

0.123 |

|

Joint estimation |

0.418 |

0.320 |

– 0.065 |

0.230 |

0.476 |

0.504 |

0.787 |

|

Discounted incremental |

0.050 |

1.394 |

– 1.394 |

– 0.295 |

0.064 |

0.577 |

1.056 |

|

Annual discount rate |

|||||||

|

Linear utility |

2.350 |

2.788 |

0.250 |

0.489 |

1.144 |

2.947 |

6.904 |

|

Discounted utility |

2.219 |

2.699 |

0.240 |

0.464 |

1.035 |

2.535 |

6.707 |

|

Joint estimation |

1.387 |

2.910 |

– 0.105 |

0.000 |

0.101 |

1.297 |

6.417 |

|

Discounted incremental utility |

2.058 |

2.936 |

0.101 |

0.306 |

0.783 |

2.616 |

6.703 |

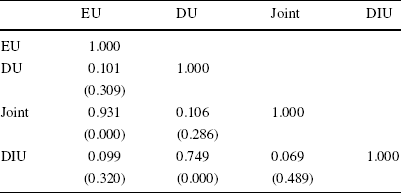

Table 6 reports the Spearman rank correlation matrix for the four individual measures of utility curvature. This strongly supports the conjecture that risk and time preferences reflect two distinct notions of utility. On one hand, the expected utility and joint estimates, which infer curvature from choices under risk, are highly significantly correlated. On the other hand, the discounted utility and discounted incremental estimates, which infer curvature from choices over time, are also highly significantly correlated. However the remaining four coefficients, which compare one measure elicited under risk to another measure elicited over time, are consistently small (Spearman rho less than 0.11) and far from statistically significant.

Table 6 Spearman rank correlation matrix of individual utility curvature estimates

|

EU |

DU |

Joint |

DIU |

|

|---|---|---|---|---|

|

EU |

1.000 |

|||

|

DU |

0.101 |

1.000 |

||

|

(0.309) |

||||

|

Joint |

0.931 |

0.106 |

1.000 |

|

|

(0.000) |

(0.286) |

|||

|

DIU |

0.099 |

0.749 |

0.069 |

1.000 |

|

(0.320) |

(0.000) |

(0.489) |

p-values in parentheses

Figure 6 depicts a scatter plot of the individual estimates of

under expected utility and

under expected utility and

under discounted utility, these being the standard normative benchmarks for risk and time preference respectively.Footnote 33 According to the model of discounted expected utility, these measures are interchangeable and so all points should lie on a 45-degree diagonal. Instead, not only do the two sets of estimates differ considerably in magnitude, they are also essentially uncorrelated.Footnote 34

under discounted utility, these being the standard normative benchmarks for risk and time preference respectively.Footnote 33 According to the model of discounted expected utility, these measures are interchangeable and so all points should lie on a 45-degree diagonal. Instead, not only do the two sets of estimates differ considerably in magnitude, they are also essentially uncorrelated.Footnote 34

Fig. 6 Scatter plot of individual estimates of

and

and

To further examine the implications of alternative assumptions regarding the nature of utility, I use each set of estimates to generate predicted choices for each subject in each of the ten risk and 60 time preference decisions, and compare these predictions to their actual choices.Footnote 35

For risk preference, simply assuming linear utility (i.e., that every subject switches from safe to risky after four rows) suffices to correctly predict 76.7% of the data. Relative to this benchmark, individual curvature estimates from the discounted utility model correctly predict 76.8% of risk preference choices, while those of the discounted incremental model correctly predict 74.6%. Treating individual subjects as independent observations, the proportion of their choices correctly predicted by either model does not differ significantly from the proportion correctly predicted by linear utility, in either a sign test or a signed-ranks test. By contrast, individual expected utility estimates correctly predict 98.5% of choices, and joint estimates 95.0%, both improving significantly upon linear utility with

in both a sign test and a signed-ranks test.

in both a sign test and a signed-ranks test.

For time preference, individual discount rates assuming linear utility correctly predict 86.6% of the data. This increases to 89.4% allowing non-linear utility in a discounted utility model, or 87.3% in a discounted incremental model. Again treating individual subjects as independent observations, both sets of estimates improve significantly upon linear utility.Footnote 36 By contrast, individual joint estimates correctly predict only 68.4% of the data. Recall that joint estimation uses only the CB choice list for time. Individual linear utility estimates using only CB data (corresponding to model (4) in Table 1) correctly predict 84.1% of the data. The individual joint estimates predict significantly worse than this linear-CB benchmark, with

in both a sign test and a signed-ranks test.

in both a sign test and a signed-ranks test.